Integrated payments connect businesses, platforms, and ISVs to third-party payment processors in order to facilitate transactions. Learn when integrated payments make sense and when to choose embedded payments for more control and revenue.

Key takeaways

- Integrated payments connect platforms to existing processors for fast setup, but limit control over payment flows and revenue.

- Platforms that scale beyond basic checkout should transition from integrated to embedded payments for monetization and customization.

- Keeping payments natively synced with business tools reduces manual reconciliation, lowers errors, and improves customer conversion rates.

Integrated payments are often the first step for online platforms, SaaS, and businesses to start accepting payments. With integrated payments, instead of building payment infrastructure from scratch; platforms connect to an existing payment processor, add checkout to their product, and start accepting transactions almost immediately.

According to a report from Bain & Company, platforms and ISVs can tap into a potential $35 trillion in payments volume (that's roughly 15% of global transactions) by integrating payments directly into their platforms.

In this guide, we’ll break down how integrated payments work, the pros and limitations of integrating payments, and how payment integration compares to embedded payments (especially as platforms scale).

What are integrated payments?

Integrated payments link your checkout and business tools to a payment processor through plugins, built-in integrations, or APIs.

When a customer makes a purchase, the payment flows through the processor while automatically syncing with the rest of your systems.

They’re usually quick to set up, which makes them a popular choice for platforms that need to start accepting payments fast – even if most end up moving toward embedded payments to gain more control over the payment flow, monetize transactions, and build payments directly into the product experience.

For example, a SaaS company using Whop can start accepting subscriptions through links, storefront tools, or APIs — with payments, revenue reporting, and customer data all managed in one place.

In a non-integrated setup, payments are handled separately from your business software. A terminal or external checkout processes the transaction, and the details then have to be reconciled manually across other tools.

Think of a small business running their store on one platform and processing payments through a separate gateway — orders and transactions have to be matched manually at the end of each day.

That separation creates extra work and increases the risk of errors. Integrated payments solve this by keeping transactions and business data in the same system, so payments, reporting, and operational tools stay automatically in sync.

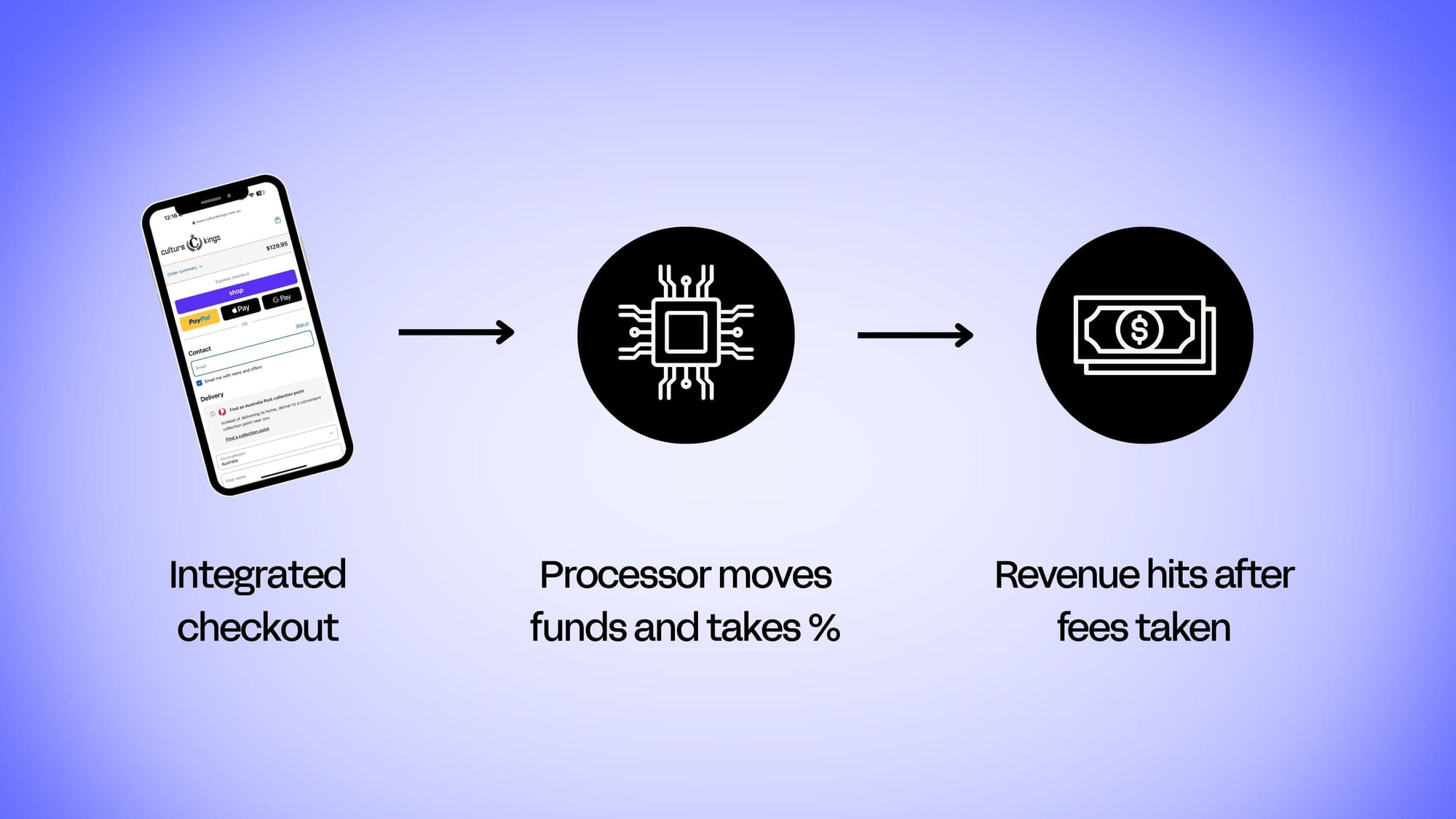

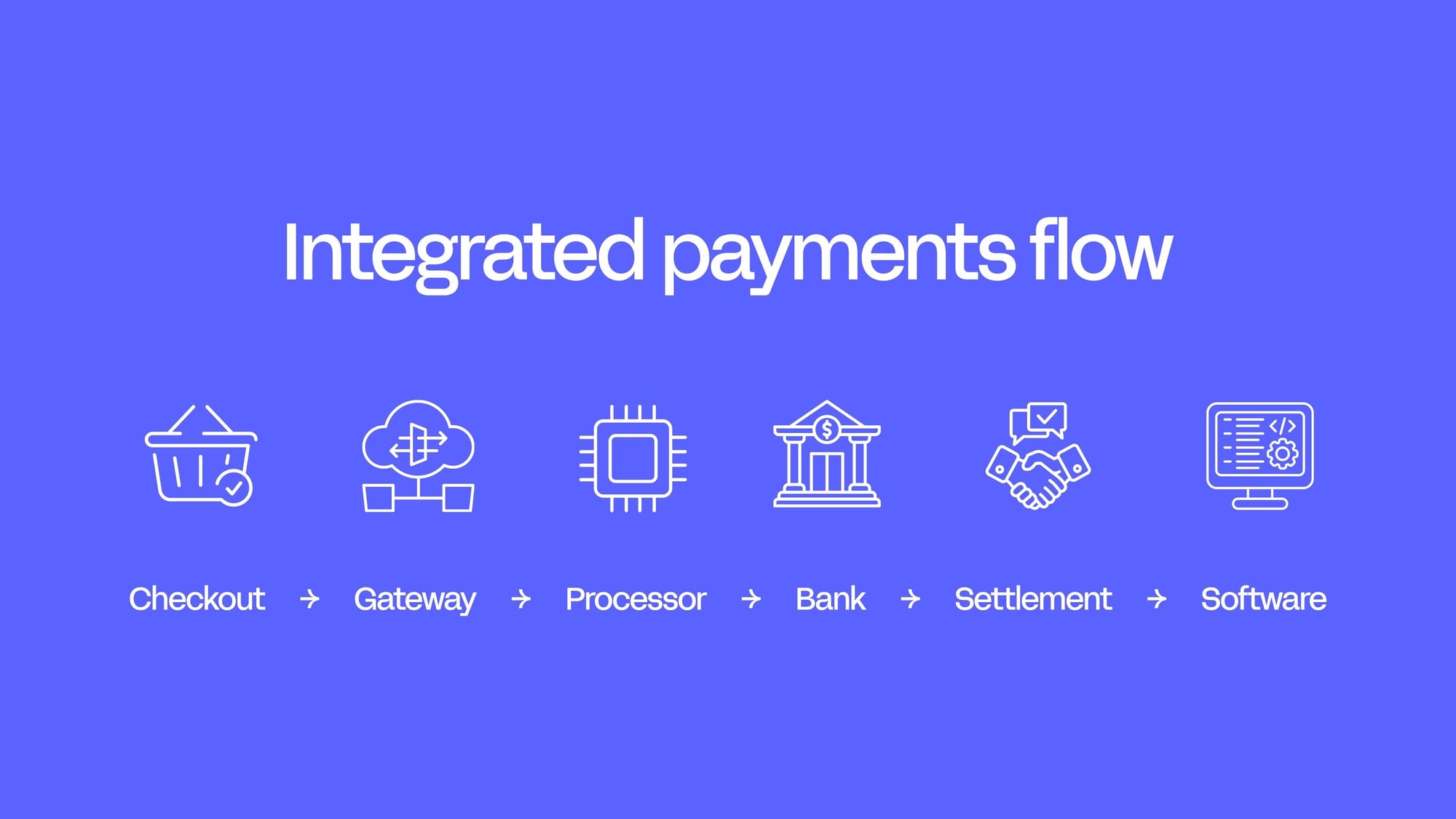

How do integrated payments work? The step by step flow

Once payments are integrated into your software, every transaction follows a structured flow between your checkout, the payment infrastructure, and the customer’s bank.

Each time a customer makes a purchase, here’s what happens behind the scenes:

Step 1: The customer initiates the payment

A customer enters their card details or selects a digital wallet at checkout in your app, website, POS system, or platform.

Step 2: The payment gateway encrypts the data

The checkout sends the payment information to a payment gateway, which securely encrypts the transaction details before sending them to the payment processor.

Step 3: The processor requests authorization

The processor sends the transaction request through the relevant card network to the customer’s issuing bank to verify the payment.

Step 4: The issuing bank approves or declines the transaction

The bank checks the account for sufficient funds and validates the card details. If everything checks out, the payment is authorized.

Step 5: Funds move through settlement

After authorization, the processor coordinates settlement. Funds are transferred from the customer’s bank to the merchant’s account, typically within one to three business days.

Step 6: The transaction syncs with your business tools

Because payments are integrated with your software, the transaction data automatically updates systems like accounting software, inventory tools, CRM records, and reporting dashboards.

APIs allow your software to send payment requests and retrieve transaction data from the processor, while webhooks send real-time notifications back to your system when events occur (such as successful payments, refunds, and chargebacks).

There are a few ways businesses can integrate payments, depending on how much control they want over the checkout experience:

| Integration type | Control | Complexity | Best for |

| Hosted checkout | Low | Low | Businesses that want the fastest implementation |

| Embedded checkout | Medium | Medium | Platforms that want branded checkout inside their product |

| Direct API integration | High | High | SaaS products and platforms needing full customization |

Pros and cons of integrated payments for platforms, SaaS, and marketplaces

Integrated payments do more than simplify checkout. When your payments are connected directly to business software, they reduce operational overhead, improve customer experience, and give companies better visibility into their financial activity.

Here's how:

Reduced friction and higher conversion

Straight up, the biggest advantage of integrated payments is that they remove unnecessary steps from the checkout process.

When payments happen directly inside a platform, customers don't need to leave the page, pull out their card, and start over — and that friction has a measurable impact on revenue.

Research shows $18B in revenue is lost yearly due to abandoned carts and checkouts, with most of those happening on mobile.

Integrated payments help reduce that drop-off by keeping the entire transaction inside the same workflow, whether a customer is buying through an ecommerce store, app, or platform dashboard.

Automated reconciliation and real-time data

Because payment systems are connected directly to business software, transaction data updates automatically across systems.

A completed purchase can instantly update their inventory levels, record the transaction in accounting software, attach the payment to a customer profile in a CRM, and update revenue in reporting dashboards.

Basically, it keeps your admin a lot easier, eliminating risk of most accounting errors.

Stronger security and compliance

Modern integrated payment systems are built with strong security standards. Payment data is protected using encryption, tokenization, and PCI DSS compliance frameworks, which reduce the risk of sensitive information being exposed.

Businesses benefit because the payment provider manages much of the infrastructure required to maintain these security standards, which can otherwise require significant time, cost, and ongoing audits to maintain independently.

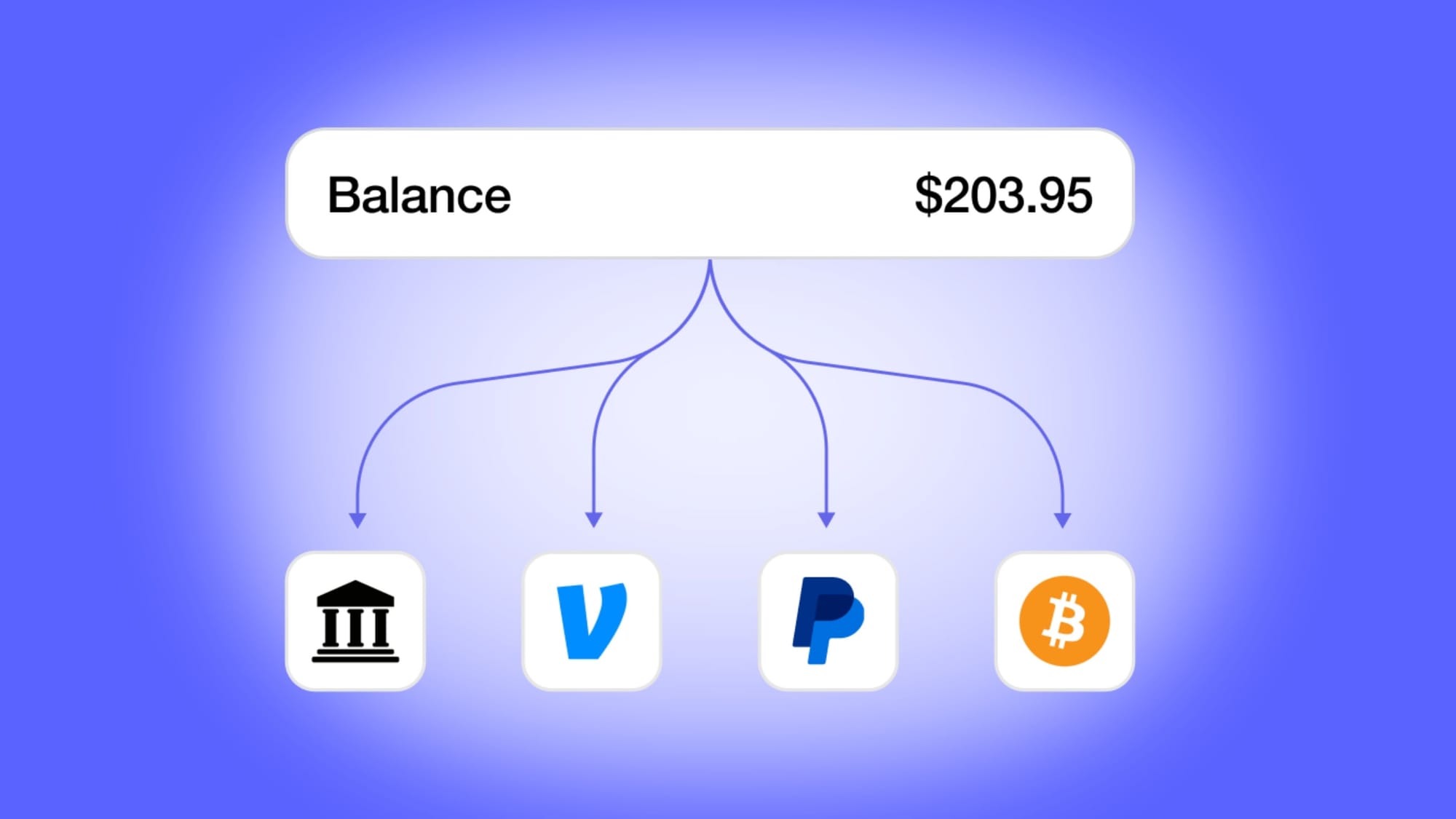

Support for multiple payment methods

Integrated payments also allow businesses to accept a wide range of payment methods without building separate infrastructure.

These often include:

- Credit and debit cards

- Digital wallets

- Bank transfers

- Buy now, pay later (BNPL) options

- Cryptocurrencies

Supporting more payment options can improve conversion rates, especially for global platforms.

Whop helps you serve more customers and improve conversion by offering the most popular payment methods around the world, with 100+ global payment methods at your fingertips.

Still, there are some downsides to integrated payments – especially compared to embedded payments. These are mainly to do with control over flows, checkout, and revenue.

| Pros | Cons |

| Fast to implement | Limited control over payment flows |

| Lower technical complexity | Processor controls much of the checkout experience |

| Built-in security and compliance | Revenue mostly captured by the payment provider |

| Automatic syncing with business tools | Harder to customize pricing and payment logic |

| Reliable payment infrastructure | Limited flexibility as platforms scale |

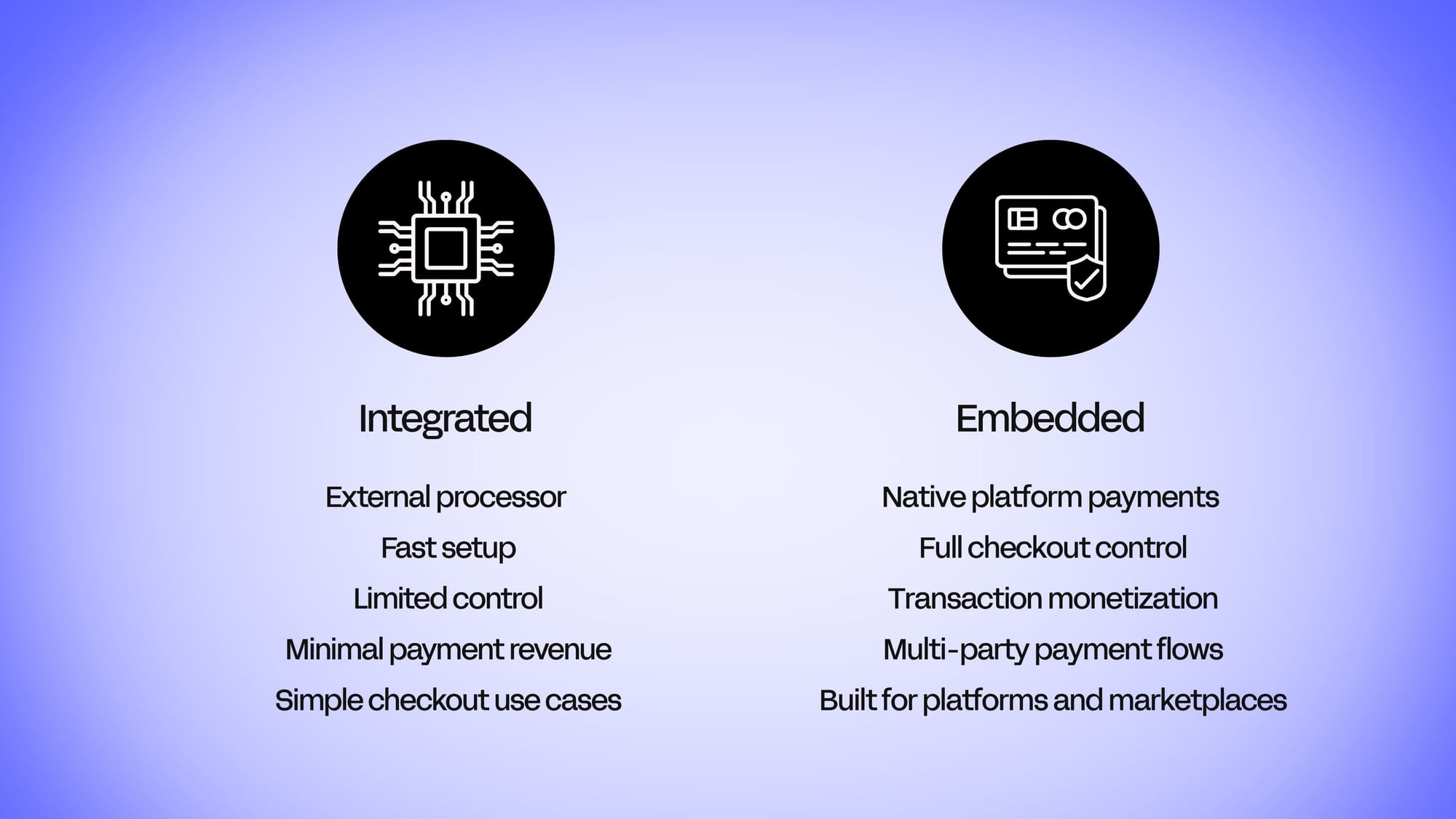

Integrated vs. embedded payments

When it comes to integrated payments vs. embedded payments, it can be confusing as the two terms that are closely related. But they actually serve different roles in a platform’s payment strategy.

As we’ve learned, integrated payments connect your platform or software to an external payment processor. Your system sends payment data to the processor, which handles most of the infrastructure behind the scenes (authorization, settlement, merchant onboarding, compliance).

The integrated payments model is popular because it’s quick to implement and requires relatively little payment infrastructure.

But embedded payments go a step further. Instead of simply connecting to an external processor, embedding makes payments a native feature of the platform itself.

This allows platforms to design their own checkout flows, manage payout routing, and capture a share of transaction fees generated on their network.

This is why many platforms who start with integrated payments later move toward embedded payment models as they scale.

| Feature | Integrated | Embedded |

| Setup | Connects to a processor | Built into the platform |

| Control | Provider controls most flows | Platform controls more of the flow |

| Onboarding | Handled by processor | Handled in-platform |

| Revenue | Processor keeps most fees | Platform can take a share |

| Checkout | Often provider-led | Native to the product |

| Best for | Fast launch | Scale and monetisation |

Why platforms and ISVs often shift from integrated to embedded payments

Integrated payments work well for traditional ecommerce, and to get platforms, SaaS businesses, and marketplaces off the ground and processing funds.

But the truth is, platforms and marketplaces with a goal of growth usually need more advanced payment capabilities than a simple checkout integration. That’s because platform transactions usually involve multiple parties, not just a buyer and a seller.

Marketplaces need to split payments between multiple sellers, send payouts to each seller’s bank account, and collect a platform fee from the transaction. ISVs and platforms need to manage connected accounts for vendors, creators, or service providers.

Handling these sorts of flows typically requires infrastructure that goes beyond basic payment integrations – and that’s where embedded payments become a key focus.

And it’s not just about processing funds, either. Platforms also face operational challenges that traditional businesses don’t. They need to onboard sellers quickly, verify identities, manage disputes between buyers and sellers, and stay compliant with financial regulations across different jurisdictions.

As a platform grows, managing these responsibilities manually becomes increasingly difficult.

That’s why platforms typically look for payment solutions that support:

- Embedded checkout experiences inside the platform

- Smart payment orchestration across multiple processors

- Automated payment splitting and routing for multi-party transactions

- Global payout infrastructure

- Built-in billing, subscriptions, and invoicing

- Merchant of Record coverage for tax handling, compliance, and chargebacks

- Seller onboarding and account management for creators, vendors, or merchants

- Fraud monitoring and payment risk management

Those features move a platform beyond simple payment integration and toward embedded payments, where payments become part of the product itself.

From there, platforms can expand into broader embedded finance capabilities, such as lending products like BNPL or financial services like wallets, yield-bearing balances, and corporate cards.

What to look for in an integrated payments provider

Choosing the right integrated payment solution isn’t just about accepting cards.

The provider you choose will affect how smoothly payments run across your platform, how easily your team can manage transactions, and how well your payment system scales as your business grows.

First, consider available payment methods: this is single-handedly one of the most important things to get right.

Customers increasingly expect flexible ways to pay, including credit cards, digital wallets, bank transfers, BNPL options, and even crypto. Multiple payment methods usually means improved conversion rates and better reach in global markets.

Speaking of, consider global coverage. If your platform operates internationally, you’ll need infrastructure that supports multiple currencies, regional payment methods, and cross-border payments across different territories.

Fee transparency is another big one. A lot of payment providers charge a mix of transaction fees, currency conversion fees, and platform charges. Understanding the full cost structure upfront helps prevent surprises as transaction volume grows.

Whop has clear, transparent pricing for pay-ins and payouts with all fees for all methods outlined on our pricing page.

And if you’re getting technical, developer experience matters too. Simple APIs, reliable documentation, and responsive dev tools can make integrations significantly easier to build and maintain.

As your business grows, your payment infrastructure should be able to handle higher transaction volumes and more complex payment flows without major restructuring.

| Feature | Why it matters | Whop |

| Multiple payment methods | Improves checkout flexibility and conversion rates | ✓ |

| Global payment coverage | Supports international customers and currencies | ✓ |

| Transparent pricing | Helps businesses predict transaction costs | ✓ |

| Developer-friendly APIs | Simplifies integrations and maintenance | ✓ |

| Security and compliance | Protects sensitive payment data and reduces risk | ✓ |

| Crypto support | Expands payment options for digital platforms | ✓ |

Get full stack integrated and embedded payments right out the box with Whop

You can use Whop like a traditional integrated payments provider, connecting checkout to your product through links, storefront tools, or APIs so you can start accepting payments quickly.

But Whop also supports embedded payments, where checkout, seller onboarding, and payouts happen directly inside your platform.

Because Whop operates as a Merchant of Record, it handles the operational side of payments (including tax compliance, VAT, chargebacks, and regulatory requirements), while the checkout experience stays native to your product.

That means platforms can start with simple payment integration and gradually move toward fully embedded payments infrastructure, without switching providers or rebuilding their payments stack.

Sign up and learn why platforms like Ohana, Sideshift, and Micro1 use Whop for their payments stack.