Learn how ecommerce payment solutions work, the different types available, and what to look for when choosing the right payment infrastructure for your business.

Key takeaways

- Multi-PSP orchestration can boost successful payment charges by 6-11% by routing transactions to optimal providers.

- Payment gateways handle customer-facing checkout while processors verify funds and move money behind the scenes.

- Choosing the right payment provider requires balancing transaction fees, global reach, and features like BNPL and tax handling.

Every sale you make online passes through a payment processor. Card authorization, fraud check, currency conversion, and final settlement happens in seconds, and when it breaks down, so does your revenue.

Global ecommerce sales are projected to grow to $7.89 trillion by 2028, so getting your payments stack right is crucial. That means making sure people can actually pay you without friction.

Choosing the right payment infrastructure means thinking beyond transaction fees. Security, compliance, global currency support, and checkout experience all determine whether your payments stack helps you grow, or holds you back.

So below, we'll walk through how ecommerce payments work, the top payment providers, and how to choose the best provider for your business.

Quick look: 5 popular ecommerce payment providers

Here's a snapshot of 5 of the most popular payment providers for online business:

| Platform | Price | Pros | Cons |

|---|---|---|---|

| Whop Payments | 2.7% + $0.30 (domestic) | Global reach, MoR, BNPL + crypto | Digital-first focus |

| Stripe | 2.9% + $0.30 (US cards) | Top APIs, global methods | Add-ons increase cost |

| PayPal | 3.49% + $0.49 (wallet) | Huge user base, fast checkout | Possible holds; complex fees |

| Braintree | Varies by method | PayPal/Venmo support, split payouts | Approval needed; complex setup |

| Apple Pay | No extra fee | Fast, secure, BNPL via Affirm | Apple-only ecosystem |

How ecommerce payments really work

Online payments appear instant, but there’s a lot happening behind the scenes to make them safe and seamless. Modern ecommerce relies on two core components: payment gateways and payment processors.

A payment gateway is the checkout technology customers interact with. It captures card or wallet details and securely transmits them for verification.

A payment processor is the financial infrastructure that communicates with card networks (like Visa or Mastercard) and issuing banks to confirm the transaction and move the funds.

Here’s what actually happens when someone clicks 'Pay':

- The customer enters their payment details at checkout

- The payment data is encrypted and sent to the payment processor

- The processor routes the transaction through the relevant card network (like Visa or Mastercard)

- The issuing bank checks the card, verifies available funds, and runs fraud checks

- The bank approves (or declines) the transaction, and sends the response back through the network

- If approved, the payment is authorised and the order is confirmed

Authorization doesn’t mean the money has moved yet. After approval, the transaction enters settlement, where funds are transferred from the customer’s bank to the merchant’s account.

Depending on the payment provider, payouts typically arrive within one to three business days.

Throughout this process, sensitive payment data is protected by multiple security layers.

- TLS (Transport Layer Security) encrypts the information as it moves between the customer’s browser, payment infrastructure, and banks.

- On top of that, most modern systems use tokenization, which replaces the customer’s actual card details with a unique, non-sensitive token that represents the payment method.

This means merchants and platforms don’t need to store raw card numbers, reducing the risk of data breaches and helping maintain PCI compliance.

Top 10 ecommerce payment providers compared

1. Whop

Whop is a global payments platform built for internet business, combining checkout, payments, and payouts in a single stack so platforms and creators can monetize without managing complex payments infrastructure.

With smart routing and multi-provider payment orchestration, each transaction is sent to the provider most likely to approve it. If a payment fails, Whop can automatically retry with alternative providers to maximize successful charges (increasing conversion by around 6–11%).

Get access to multiple global and region-specific payment methods including cards, digital wallets, buy now pay later, and crypto.

Plus, pricing is simple: there’s no monthly subscription, and payments start at 2.7% + $0.30 per transaction.

Because Whop operates as a Merchant of Record (MoR), it also handles much of the operational complexity behind online transactions, including compliance, fraud monitoring, and tax obligations such as sales tax, VAT, and GST.

Running a platform or marketplace? Payouts are just as flexible. Send funds globally using bank transfers, crypto, and popular peer-to-peer payment methods, with coverage across more than 240 territories.

“Through thousands of conversations, we’ve learned our customers really only care about two things: getting paid and paying out. Our mission is to be the best in the world at solving those problems.”

- Hunter Dickinson, Head of Partnerships at Whop

Key takeaways:

- Price: Free to start; 2.7% + $0.30 per successful domestic card charge (enterprise rates available at $50K+ monthly)

- Pros: Global reach (195/135+/100+), orchestration uplift, MoR tax handling, BNPL + crypto, rich product gating, 24/7 human support

- Cons: Best fit for digital-first and hybrid businesses; not a full warehousing/logistics suite for large physical catalogs

2. Stripe

Stripe is a developer-first payments platform with modern APIs, no-code tools, and global coverage. It supports cards, wallets, bank debits/transfers, and BNPL, and bundles strong subscription and invoicing features—great for startups through to enterprises. Standard US online card pricing is 2.9% + 30¢ per successful charge (other methods vary).

Stripe also offers add-ons like Billing, Tax, and Adaptive Acceptance; these can improve revenue and compliance but may add extra cost depending on plan and region.

Stripe key takeaways:

- Price: US online cards typically 2.9% + 30¢; other methods/regions vary. Custom pricing available for large volumes.

- Pros: Excellent APIs and docs, broad global methods, robust subscriptions/invoicing, fast setup

- Cons: Add-ons (Tax, Billing tiers, etc.) can raise total cost; MoR/tax remittance not included by default

3. Paypal

PayPal brings a huge consumer wallet and one-tap checkout that many buyers recognize and trust—plus support for Venmo and standard card processing via PayPal Checkout.

Current US commercial pricing lists PayPal Checkout at 3.49% + a fixed fee (USD fixed fee is $0.49) and standard credit/debit card payments at 2.99% + a fixed fee; international adds +1.5%. Details vary by product.

Do note: PayPal may place holds or reserves on merchant funds in certain risk scenarios (new sellers, high disputes, industry risk, etc.). That's good for buyer protection, but can be frustrating for cash flow.

PayPal key takeaways:

- Price: Typical US rates include 3.49% + $0.49 for PayPal wallet/Checkout and 2.99% + $0.49 for standard card payments; plus +1.5% on international

- Pros: Enormous wallet adoption, fast checkout, flexible options (PayPal, Venmo, cards)

- Cons: Possible account holds/reserves; fee tables can be complex across products

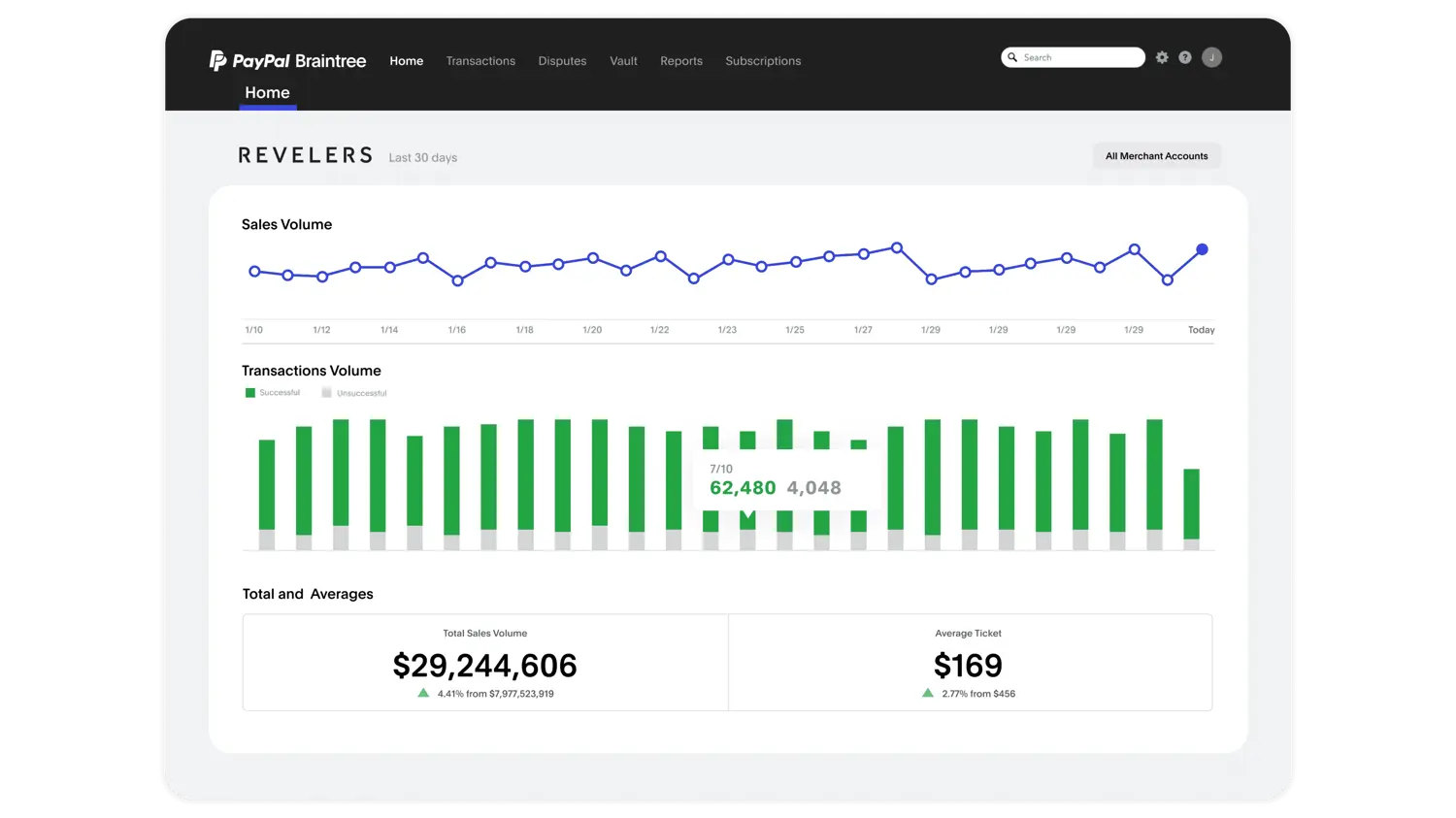

4. Braintree

Braintree (a PayPal company) is a full-stack payments platform and gateway built for web and mobile.

With a single integration, you can accept major cards plus PayPal, Venmo (US), Apple Pay, Google Pay, and selected local methods.

Braintree also supports split payouts via its Marketplace program, but it requires specific approval under a Marketplace Service Provider agreement. This keeps the feature set powerful while adding the compliance guardrails marketplaces need.

Pricing is method-specific and varies by region, risk profile, and product (cards vs. wallets vs. local methods).

PayPal publishes Braintree's fees and notes that they can differ by merchant; confirm your exact schedule on the fees page or with sales.

Braintree key features:

- Price: method-specific; see PayPal's Braintree fee tables for your region and products

- Pros: native PayPal/Venmo/wallet support, marketplace split payouts (with approval), strong PCI posture (Level 1), global reach with multi-currency

- Cons: marketplace requires approval; fee structure can be complex across methods/regions; PayPal ecosystem policies (e.g., reserves/holds) may apply depending on risk profile

5. Apple Pay

Apple Pay is a digital wallet that lets customers pay using the card details stored on their Apple devices. Instead of typing card information at checkout, shoppers can approve a payment instantly with Face ID, Touch ID, or their device passcode.

Behind the scenes, Apple Pay uses tokenization: the customer’s real card number is never shared with the merchant. Instead, a secure payment token is sent through the card networks and processed like a standard card transaction.

For ecommerce businesses, Apple Pay is typically enabled through a payment provider or checkout integration (like with Whop). Once activated, it appears as a one-tap payment option in supported browsers and apps on Apple devices.

Because checkout happens in seconds and doesn’t require manual card entry, Apple Pay can significantly reduce friction on mobile and improve conversion rates (especially for mobile shoppers).

Check out our documentation to add Apple Pay to your Whop embedded checkout!

Apple Pay key takeaways:

- Price: no separate Apple fee; you pay your processor's standard card/wallet rates

- Pros: faster mobile checkout, biometric authentication, network tokenization (card numbers aren't shared with the merchant), broad global availability, optional BNPL via Affirm (U.S.)

- Cons: limited for non-Apple users; Apple Cash P2P is U.S.-only

6. Google Pay

Google Pay is Google's digital wallet for Android and Chrome users. It lets customers store cards, passes, and loyalty points, and pay online or in-store with a tap. In many markets, Google Wallet stores the payment methods, while Google Pay handles the actual transactions.

Transactions are secured with device-level authentication—PIN, password, or biometrics like fingerprint or face unlock—so checkout feels seamless but still safe. It also supports peer-to-peer payments in certain regions, though its primary strength is ecommerce and mobile commerce.

Adoption is climbing steadily, with more ecommerce stores adding it alongside Apple Pay to capture mobile-first buyers.

Google Pay key takeaways:

- Price: No separate Google fee; you pay your payment processor's wallet/card rates

- Pros: Built-in for Android users, fast tap-to-pay online and in-store, strong device security, loyalty integrations

- Cons: Limited to Android/Chrome ecosystem; availability and feature set vary by country

7. Amazon Pay

Amazon Pay leverages Amazon's massive customer base, letting shoppers use their stored Amazon credentials to check out on third-party sites. That means fewer abandoned carts, especially for Amazon-heavy users who trust the brand.

It supports one-time and recurring payments, integrates easily with ecommerce platforms, and offers Amazon's familiar interface at checkout. Merchants benefit from both trust and speed—customers don't need to create a new account or re-enter card details.

Availability is region-based, offered in countries including the US, UK, Germany, Japan, and India. Adoption is growing, but it's not as universal as wallets like PayPal or Apple Pay.

Amazon Pay key takeaways:

- Price: Processor-dependent; generally aligned with card transaction fees (check your provider).

- Pros: Huge consumer trust, frictionless checkout for Amazon account holders, recurring payments support.

- Cons: Limited to supported regions; not as flexible for merchants outside Amazon's ecosystem.

8. Square

Square (a Block, Inc. brand) started as a simple card reader but now powers millions of businesses with POS hardware, online stores, invoices, and APIs. It's especially strong for sellers who operate both in-person and online.

Square has transparent pricing: in the US, 2.6% + 10¢ per in-person tap, dip, or swipe, and 2.9% + 30¢ for online transactions. It also supports cards, wallets (Apple Pay, Google Pay), ACH bank transfers, and gift cards.

Since acquiring Afterpay, Square lets merchants offer BNPL both online and in-person. Customers pay in installments while sellers get paid upfront (minus the Afterpay fee).

Square key takeaways:

- Price: US in-person 2.6% + 10¢; online 2.9% + 30¢. Custom enterprise rates available.

- Pros: Best-in-class POS hardware, strong online store tools, built-in BNPL via Afterpay, easy for hybrid businesses.

- Cons: Primarily US-focused; less global reach and fewer currencies than Stripe or Whop.

9. Klarna

Klarna is one of the biggest names in buy now, pay later (BNPL). Its core offerings: Pay Now, Pay in 30 Days, Pay in 3 or 4 Installments, and financing for larger purchases. These options can boost conversion rates and average order value for merchants.

Klarna integrates easily with major processors like Stripe (via Checkout or Connect), though it uses a redirect flow—shoppers complete payment on Klarna's page before returning to your site. That extra step can impact conversion, but many customers already know and trust Klarna.

It's available in 45+ markets and claims hundreds of millions of active users globally, making it a strong option if your buyers expect BNPL.

Klarna key takeaways:

- Price: Varies by region and product; typically a per-transaction fee plus a fixed charge.

- Pros: Familiar BNPL brand, boosts order value, broad market coverage, Stripe/Braintree integrations.

- Cons: Redirect checkout flow adds friction; fees vary; not all buyers want installment payments.

10. Adyen

Adyen is a global PSP that offers payment processing, acquiring, and risk management; allowing businesses to accept online, mobile, and in-person payments while handling authorization, settlement, and reporting.

For ecommerce, Adyen typically sits between the checkout experience and the card networks. When a customer submits a payment, Adyen routes the transaction to the appropriate card network or local payment rail, communicates with the issuing bank to approve the charge, and settles the funds to the merchant.

However, Adyen is still just one provider within the payments world.

Most platforms and marketplaces connect multiple PSPs or use orchestration layers so they can route transactions between providers, improve authorization rates, reduce downtime risk, or optimise fees across regions.

Adyen key takeaways:

- Price: Card fees start around interchange + 0.6% + $0.12 per transaction – no monthly fees, though a $120 minimum monthly invoice may apply depending on volume.

- Pros: Global reach, many supported payment methods, flexible APIs.

- Cons: More complex setup for small businesses; higher minimums make it less friendly for early-stage sellers.

What makes a good ecommerce payment solution?

Choosing a payment provider isn’t just about processing money.

The right infrastructure improves checkout conversion through faster, smoother payments, expands your global reach with local methods and currencies, reduces operational overhead by automating compliance, fraud, and reporting, and supports scaling as transaction volume and payout complexity grow.

Here's how to make the right choice:

Checkout performance and conversion

Checkout structure has a direct impact on conversion.

Integrated checkouts redirect the customer to a payment page hosted by the provider. They’re quick to set up and handle most security and compliance automatically, but the redirect adds friction and breaks the checkout flow.

Embedded checkouts keep the payment fields directly on your site or inside your product. Customers can enter their details, use wallets like Apple Pay, and complete the purchase without leaving the page.

Because the experience is smoother and faster, embedded checkouts often convert better, especially on mobile.

Security and compliance

Handling payment data means dealing with strict security standards. Reliable payment providers maintain PCI DSS compliance, encrypt data in transit using TLS, and rely on tokenisation so merchants never store raw card details.

Beyond protecting customer data, modern payment systems also include fraud detection and risk scoring to identify suspicious transactions before they become chargebacks – which can erode profit and reputation.

Maddie Cohen tells us that chargebacks typically happen when customers can't find a clear path to resolve issues directly with merchants. Whop addresses this with a defense system:

- The Resolution Center prevents chargebacks before they reach banks

- Dispute fighter automates your response if a chargeback does occur

Global payment coverage

If you sell online, your customers may come from anywhere. A strong payment solution supports multiple currencies and a wide range of payment methods, including cards, digital wallets, and local payment options that shoppers in different regions expect to see.

Without those options, international customers often abandon checkout simply because their preferred payment method isn’t available.

Pay-in and payout infrastructure

Accepting payments is only half the equation. Businesses also need a reliable way to receive the funds after a transaction is approved.

For most ecommerce merchants, this simply means payments settling into their bank account after a short payout window. But for platforms, marketplaces, and creator economies, payments are more complex. They may need to split revenue between multiple sellers, schedule payouts, or send funds across borders in different currencies.

In those cases, payout infrastructure becomes just as important as checkout itself.

Whop pays out in over 241+ countries & territories via ACH (bank deposit), Crypto, Venmo, CashApp and more.

Pricing transparency

Most payment providers charge a percentage of each transaction plus a small fixed fee. While the headline rate is important, businesses should also pay attention to cross-border fees, currency conversion costs, chargeback fees, and any platform-specific pricing tiers.

Clear pricing structures make it easier to predict margins as transaction volume grows.

Reliability and support

Payments are critical infrastructure. If your provider experiences downtime or failed authorizations during peak traffic, the impact on revenue can be immediate.

Reliable platforms maintain high uptime and provide responsive support teams that can quickly resolve issues with payments, payouts, or integrations.

How ecommerce payment solutions impact your business

Choosing the right payment solution directly impacts your sales, your customers’ trust, and even your ability to grow. Here are the key areas where payments make a difference:

| Area | What it affects |

|---|---|

| Checkout flow | Embedded checkouts keep customers on your site, while redirects add friction that can reduce conversions. |

| Payment approvals | Providers route transactions differently, which can affect how many payments get approved. |

| Global payments | Support for local payment methods and currencies helps international customers complete purchases. |

| Payouts | Settlement speed and payout options determine how quickly you receive your revenue. |

| Risk management | Fraud tools and compliance systems protect against chargebacks and payment disputes. |

| Reliability | Payment uptime and infrastructure determine whether customers can successfully complete purchases. |

Process ecommerce payments and platform payouts with Whop

The right payments stack is often the difference between customers checking out or bouncing.

Most payment processors connect you to a single provider. Whop sits above that layer, connecting you to multiple partners behind one integration, so transactions can be routed through the infrastructure most likely to succeed.

Accept payments from customers in 195+ countries using more than 100 payment methods, including cards, wallets, BNPL options, and crypto. That means customers can pay the way they expect to, wherever they are.

Whop also operates as the Merchant of Record, taking on things like sales tax, VAT, and other compliance requirements on your behalf.

And unlike most payment processors, Whop also runs a marketplace where businesses can list their products and reach warm buyers.

Plus, if something goes wrong, support is available 24/7 from a real team.

Power your sales with Whop Payments: no middlemen, no friction, more profit.

Ecommerce payment FAQs

How does payment processing work with ecommerce?

When a customer checks out, their payment details are encrypted and sent through a payment gateway. A processor then talks to the card network, the customer’s bank (issuer), and your bank (acquirer) to authorize the charge and move the money.

How are ecommerce payments made secure?

Modern payment solutions use TLS encryption (the successor to SSL) to secure data in transit, and PCI DSS compliance to keep card details safe. On top of that, most platforms now use tokenization—replacing sensitive data like card numbers with non-sensitive tokens—so the raw details are never stored on your systems.

What is the difference between a payment gateway and a payment processor?

Think of the gateway as the customer-facing part (checkout page, Apple Pay button, PayPal pop-up). The processor is the behind-the-scenes engine that authorizes the charge, verifies funds, and moves money between banks. They work together, but they do different jobs.

Do I need a payment processor for my ecommerce store?

Yes. Every online store needs a processor to handle the movement of funds securely between customers and merchants. Many platforms (like Whop, Stripe, or Braintree) bundle the gateway and processor into one so you don’t have to set them up separately.

What are transaction fees?

Every processor charges per transaction, usually as a percentage of the sale plus a flat fee. In the US, standard card rates are around 2.7–3.5% + $0.30. Rates can vary by payment method, country, and volume—some platforms offer discounts at higher processing levels.

Does a payment processor or gateway collect taxes?

In most cases, no—you as the merchant are responsible for collecting and remitting taxes like VAT, GST, or sales tax. The exception is when you use a provider that acts as Merchant of Record. For example, with Whop Payments, Whop is the Merchant of Record, so taxes, compliance, and remittance are handled automatically.